Passive Saving for Parents

Do you struggle to find extra money at the end of the month to put into savings.

Do your kids seem to soak up all the money you ever have?

You need ways of saving that are quick, efficient and don’t take up too much time.

By reading this post you will learn:

- What are the important things each family might save for

- Passive Saving for Parents – 3 saving strategies and how to put them into action today!

I know that everyone that reads this post has a different situation. Some are relatively well off. Some are not. Some have money to set aside every month. Some are living week by week and having to go to food banks as the Universal Credit scheme has left them really struggling.

At the end of this post I hope you will consider yourself better prepared reach your family money saving goals.

If you’re struggling to keep any money aside to save, I hope that our other articles can help you. We have posts on maximising the free childcare you can claim, saving money on essential products, parental leave and lots more. Take a look at our Start Here page to find out more.

How to Start Saving

I know you’re eager to save, improve your finances and build a stable home to bring up your kids.

First things first though, we need to have a few things in place before and alongside your savings.

Do these things first

- Pay off credit card or high interest debt.

- Ensure you have enough in the account to pay off your financial commitments (mortgages, rent, loans, bills) for that month.

Your next savings goal

- Save for an emergency fund

Then

- Save for your family’s future

I believe that if you read this post you will gain strategies to begin saving more money and improve your finances.

Your main goal – before any savings begin

Your main monetary goal should be that you never ever ever default on any loan, mortgage, rent, credit card or other financial product as this will seriously harm your credit rating. This means you might have trouble applying for financial products or financial help in the future. You need to make sure you have enough money in the relevant account at any one time.

This means making a budget. You can download our Family Budget worksheet from our Start Here Page.

You must know where your money is going every month. This way you’ll see where your unnecessary expenses are and where you can start to cut things out.

Have a new ‘zero’ in your account

You could approach this by trying to never have less than a certain amount in your account. You could just be really organised with the dates in which money is paid into your account and taken out (but you have to be on the ball).

Say you’ve done really well and have built up a £2000 emergency fund over the last several years. This is sitting in your instant access savings account. Why not transfer £500 of it to your current account and then run a strict rule of £500 being your new zero. Then you have a buffer against accidentally running into your overdraft and the fees that go with it. If you don’t then touch the £500 for purchases it’s still acting as money saved for a rainy day.

You could do this even if you don’t have the emergency fund built up yet. You could set your new zero at £100 or £200. It can be hard to stick to this though. You need to be firm with yourself and not go under your new ‘zero’.

Saving for your family emergency fund

How long could you manage without your current income? Could you cover a large unexpected expense. You need a cushion of easily accessible cash.

I’ve built up my emergency fund through monthly savings that come out on the first of every month with my other bills. This is a sort of passive saving in that I don’t have to make the payment. I don’t really notice it.

I’ve been paying into mine for a few years and now it’s relatively healthy, I treat it as one of the core ‘bills’ like the mortgage and council tax. How much you pay in is up to you and can vary depending on your situation and the time of year. I do change it so I pay in less in december and january than i do in the other months.

I’m writing a post all about emergency funds and with tips on how to prioritise it and maximise the amount you put away. It’s coming soon!

What else are you saving for?

What are the other things you might need to save for?

Paying off debt, car loans or home improvement loans.

Try and get down any credit card or other high interest debt (payday loans!) first.

Try an online credit checker to assess your credit score. They have handy tips on how to improve it.

A big purchase such as a new car or new kitchen is something you pay back over several years for. Most people will buy these items on credit and pay it back later. It would be wonderful to be able to buy such an item outright but not many of us can.

A lot of consideration needs to be taken over the affordability. A new kitchen might add to your house value if you own it.

A new car will only depreciate. I regret spending a lot of money on my beloved BMW when I was 23!

Christmas

If you’re very organised, have a savings pot from early in the year to cover presents (and also birthday presents). I keep a cash savings pot in a money box at home for presents.

I will add to it whenever I can throughout the year.

Children’s savings fund.

Putting just £20 a month in a savings fund for your child will build lots and lots of compound interest over their 18 years. You can get children’s savings accounts with interest rates of around 4%.

Assuming the interest rate stays the same for 18 years:

- £20 a month in such an account will be worth over £6300

- £50 a month in such an account will be worth over £15000

- £100 a month in such an account will be worth over £31000

Holidays

This is a big expense that needs longer term planning for. You should see the monthly saving for holidays as a core bill. My wife and I have a separate pot in our joint account called the ‘Holiday Fund’ to which we make standing orders every month.

Pensions

Do you have a workplace pension?

If not, can you afford to save for a private pension rather than just rely on the state one? The state pension does not give you a lot of income if it’s your only source of income in retirement. The age at which you can claim seems to be climbing regularly too.

I would recommend getting some professional advice about pension savings if you don’t have one with work.

Strategy 1 – Substitute an unnecessary item for Savings

Cut out an unnecessary item and save what you’d have spent.

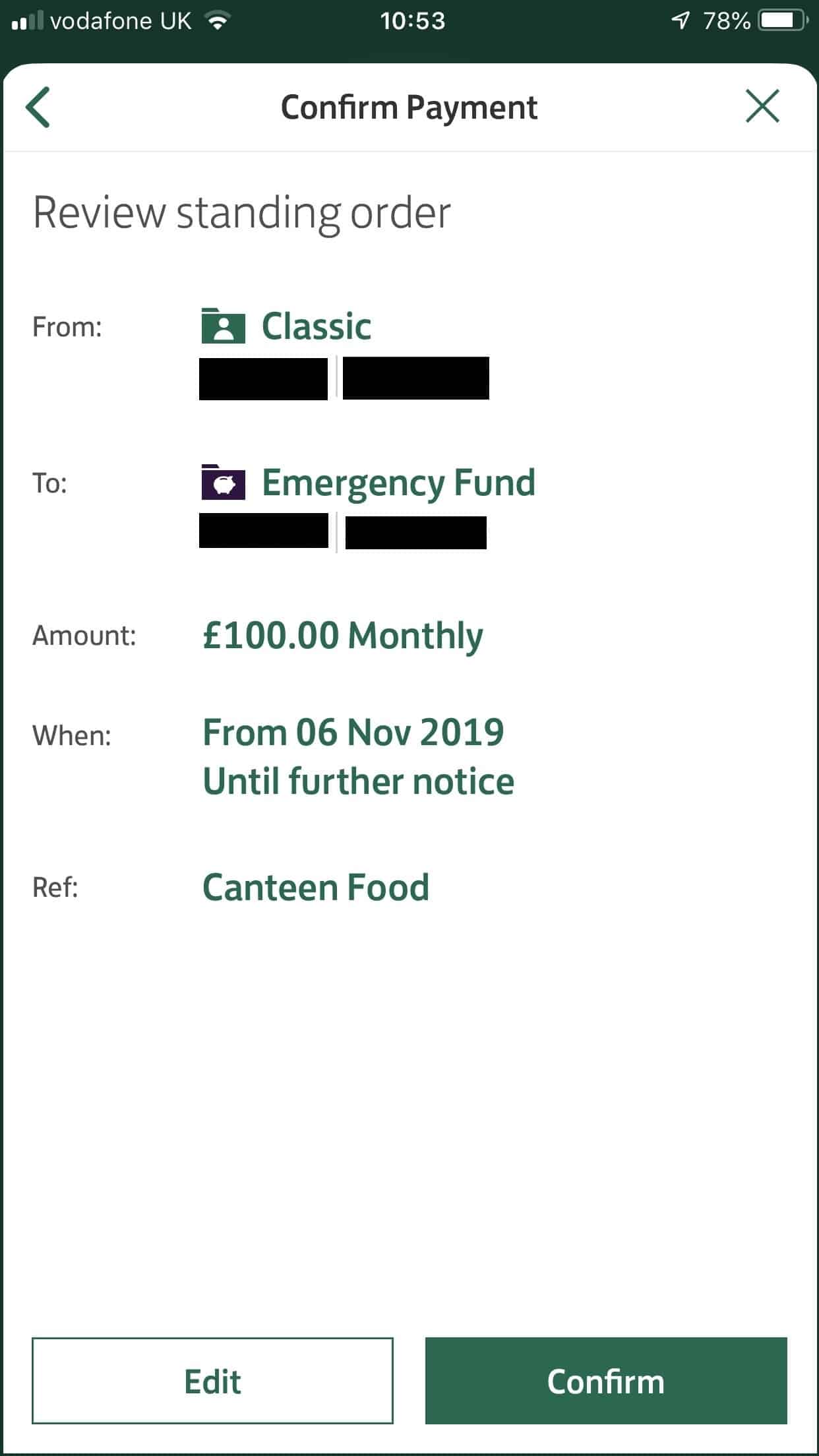

I used to spend a fortune on hospital canteen food and vending machine fizzy drinks. This was unhealthy and cost me £5 or so per day (around £100 per month). I stopped this 18 months ago and put the £100 per month towards my emergency fund.

I have a regular payment set up from my current account to the emergency fund account with the reference ‘Canteen’. Like me, this account is now healthier and I’m glad I did it. Of course I’ve spent some extra money on the packed lunches I’ve taken to work but it’s much less. I often take soup or leftovers from the night before.

You can do the same by getting rid of a subscription you don’t use (magazine/sky tv etc) and setting up the payment to your savings fund with the name of the thing you stopped paying.

I’d like to do the same with fizzy drinks, which I drink far too much of. That’s my next goal. I’ll call the payment reference ‘fizzy pop’.

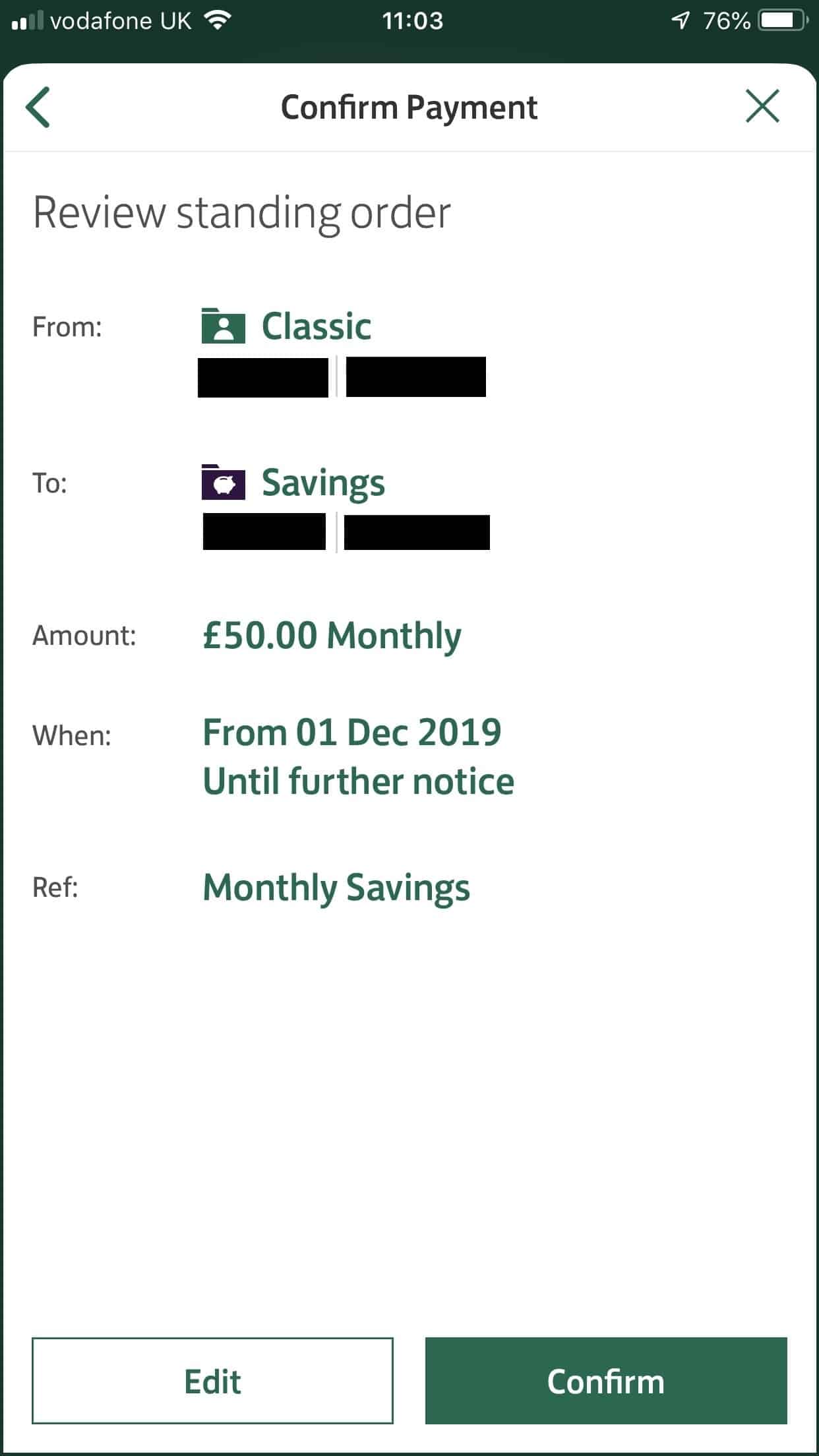

Strategy 2 – Pay yourself first

This is a common way of saving. When you’re paid and your rent/bills go out, set up a regular payment to your emergency fund/savings account to go out without you thinking about it.

Use these action steps today to organise your monthly bills.

- Identify all the regular bills that come out of your current account each month and write them down.

- Assemble all the phone numbers of the companies that you pay.

- Ring them all up one by one and change your direct debit payment to the 1st of the month. This way you’ll be paid at the end of the previous month, all your bills will come out on the 1st and you’ll then be able to see where you stand. You wont have to worry about the electric bill coming out on the 25th of the month when you’re running low on funds.

- Set up a regular payment from your current account to your savings fund for the 1st of the month. It will go out with your other bills and you won’t notice it as much. I have a lower limit that I want to see in my account after all bills and savings have been made. This is to cover all the purchases i’ll make in the month. The savings payment should be your remainder after bills, minus the money you need for the month. Creating a family budget will help you know how much you need.

- If you’re struggling later in the month you can lower the value of your regular savings payment for next month.

This way means you don’t leave the savings payment til the end of the month when you have nothing left.

Strategy 3 – A round-up app

Round up all your transactions to the nearest pound

I use a great saving app called Moneybox.

This is my method of saving for the long term and my Moneybox account is not my emergency fund. This is because it takes a little bit of time to access the money if I want to make a withdrawal.

It is a stocks and shares ISA linked to my bank account. I log onto it and it shows me what I’ve spent on the debit card and credit card that month. I can then swipe to round that amount up to the nearest pound with the difference being sent to my moneybox ISA account. You can round up as many or as few transactions as you like. You can also have double round ups and add regular or one off amounts depending on how much you have to save.

You choose your investment outlook from three options (cautious, balanced, adventurous). Obviously this comes with warnings that your capital is at risk. Moneybox then takes care of the investment decisions for you. For me, it is a good way of saving passively whilst putting some of your money in the stock market. This seems to me like a good way of saving over the long term where stocks may do better than cash accounts.

Note you can have a cash ISA and a separate stocks and shares ISA in the same financial year in the UK, but you can only pay in a combined £20,000. Since the latest changes to these rules in 2018-19 you can pay in up to £20,000 into just one or split it between them. Well done if you’re able to max out this threshold, most people can’t!

There are apps and accounts available that round up your transactions from your bank account, but don’t invest them in stocks and shares.

Please be aware this site and author are not giving professional financial advice. Before making financial or investment decisions you should research the topic in full and consider taking professional advice. As I use this app I am aware that the money/capital I put into it is at risk.

JamesGetting your kids in the habit of saving

We’ve created a whole post on Teaching you kids about money. Within this article I talk a lot about how to nurture the habit of saving money in your children. There are strategies for young children, school age and teens.

Conclusion

Set some easy savings goals, achieve them and keep going!

I hope you can put some of these strategies into action and improve your financial situation by the end of the next year. They really work great for me and my family.

Set yourself some goals for 6 months time and see how you get on. Make these easily achievable and break them up into chunks. If your goal was to save £500 in a year make it £250 by six months time and work hard towards it. Reaching targets you’ve set can be really motivating. If you make your £250 target the £500 will be easier to strive for.

I hope this post has helped build your confidence with saving. Please share this article with your friends if you found it helpful!

Thank you for taking the time to read this post.